4th Quarter,

2001

December 31,

2001

Since our model portfolio

started during the last quarter of the year, this quarterly report will

also be our year-end report.

The first reporting period of

our model portfolio coincided with a major turning point in the U.S.

markets. After the terrorist attacks of September 11, the markets, already

plunging, entered into a free fall, leading to the recent lows on

September 21. The following week a strong and volatile rally started. Over

the following weeks, the major indexes staged a series of follow through

days,

(as defined by Investor's Business Daily) confirming the new direction.

Our system, being based upon

the concept of market confirmations (as opposed to market predictions,

which are based on opinions), will always be "late" in its

entry, because, at turning points, we wait for our trend indicators to

signal the new trend in its weekly study. Furthermore, one of our core beliefs

that says that it is necessary to give some gains back in order to capture potential

big moves, make us not to attempt jumping at the top. We always wait

for the market to trigger our stops. This might be perceived as a drawback

that inevitably leads to underperformance. However, one of the key

features of our system is that it enters the markets when the downside risk

is at its lowest, and exits them when the risk of cutting our gains short

is at its lowest. Additionally, our system will keep most of our gains

during periods of adverse conditions.

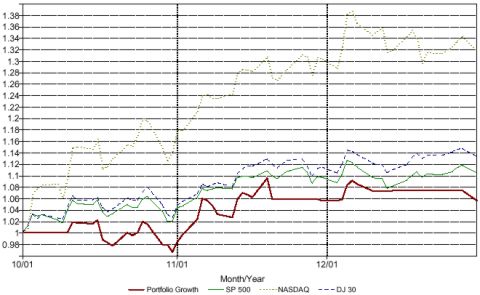

During most of this quarter,

the market has been in an up-trend mode, although with wild volatility.

The performance of our model portfolio was negatively impacted by initial

errors in the implementation of the system. Mainly, a last minute

adjustment in stops management. Changes that were not part of the

preliminary study and therefore introduced doubts at moments in which

swift and decisive action was needed. Another big mistake involved a lack

of discipline in the execution of trading signals. Although this last

issue can be solved by the means of using stop orders (with higher

commissions), it reveals that personal improvement is necessary.

Discretional exits were used

during the Thanksgiving long weekend, and during the year-end holiday, as

the portfolio manager went on vacation. At the end of November, a

non-regular deposit in the mid 3 figures was made. As noted in the allocation chart,

the period ended with the account balance 100% in cash. The drop at the

end of the performance chart reflect the impact of the management fees on

the portfolio.

Trading watch will

resume on January 2, 2002. Happy New Year!