2nd Quarter,

2002

June 28, 2002

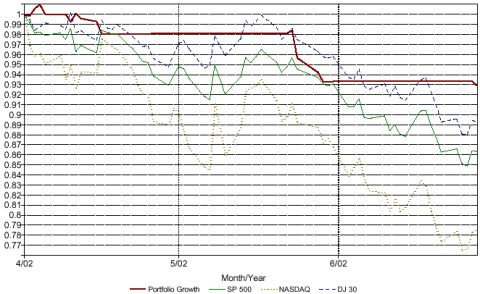

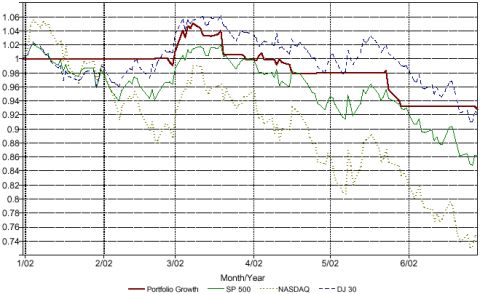

The dull 1st quarter was

followed by an interesting one. The results of our initial experiments with short selling were

not exactly good and we decided to sit out the slide for the rest of the

downtrend. However, since it is our belief that our system can be used on

the short side, we kept experimenting short selling on paper and we will resume using

in right after the next up-trend tops. On late May a rally attempt failed,

dragging down our portfolio about 5%. However, our system kept the

losses to a minimum and by the end of the quarter we are outperforming the

S&P 500 by 6.54% even after management fees. For the year, our portfolio

is doing 6.61% better than the big cap index. While having a negative

return is nothing to be proud of, we are satisfied with the relatively low

risk we are taking, considering that we use leverage up to the maximum

amount allowed, in accordance with the position sizing algorithm of our

system.

During this quarter we also

made a review of our stop monitoring system used during the last quarter

of 2001 and decided to make some adjustments oriented to give our trades

more room to jiggle, thereby reducing churning and increasing the

possibilities to have larger reward/risk ratios. Another change that was

introduced will affect the periodicity of the charging of profit fees.

Currently this fee is charged at the end of the quarter. From now on, it

will be charged once a year, 2 business days prior to the last business

day of the fiscal year-end for the Fund, December 31.